I have been ‘mapping’ the local Brazilian Distressed/Special Situations/High-Yield market for some time and will start a small series with specific topics – this is the first post – an introduction.

The intention here is NOT to cover all legal aspects – this is a practical introduction to anyone interested in Brazilian restructurings, distressed debt/special situations (and is probably analyzing now OGX,OSX, Lupatech, and Aralco among others).

A couple of data points:

–Total credit expanded over 500% in the last 10 years – as of January, 2014 it reached 56.1% of GDP – BRL $2.7 trillion (~USD $1 trillion),

–Corporate Credit represents roughly 54% of the total – average tenor (corporate credit) went from 5.7 months to 30.1 months,

-As of June,2013 – the 4 largest local banks held 74% of all credit,

-From April,2013 to March, 2014 the base local overnight rate (Selic) has climbed 300 bps to 10.75% p.a.

The ‘New Brazilian Bankruptcy Law’ (Law. 11101 dated February 9th, 2005) provides three procedures to address failing companies: (i) ‘Recuperação Extra-Judicial’ or out-of-court reorganization – a rarely used simplified procedure that does not includes ‘automatic stay’ or Trustee supervision, (ii) ‘Recuperação Judicial’ or Judicial Reorganization – that emulates Chapter 11 of the U.S. Bankruptcy Code and (iii)‘Falência’ or Liquidation – similar to Chapter 7 of the U.S. Bankruptcy Code.

State-owned entities and financial services companies (including Banks and Insurance companies) are NOT covered by the ‘New Brazilian Bankruptcy Law’.Local banks usually go from Central Bank intervention, followed by ‘Liquidacao Extrajudicial’ (out-of-court liquidation) also coordinated by the Brazilian Central Bank (a recent case here).

Brazilian Bankruptcy regulation was ‘inspired’ by US Bankruptcy law – but unlike the U.S. Bankruptcy Code’s Chapter 15 – there is no mention of foreign creditors on the Law – the track record of local courts decisions on the issue (as per the recent cases of Independencia and OGX) does not indicate a clear path to include (or not) overseas subsidiaries/foreign investors in the Brazilian Bankruptcy case.

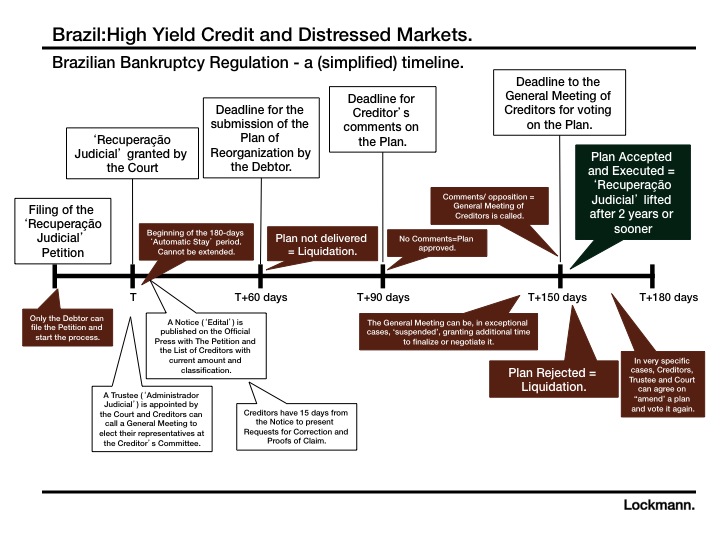

Below is a simplified schedule of a local Bankruptcy case (click to enlarge) and a couple of comments on the process:

•Recuperacao Judicial (‘RJ’) can only be filed by the Debtor and the Petition has to be filed in the Company’s main place of business and overseen by local court/judge – regardless of previous experience – with the possible exception of Rio and São Paulo that has two bankruptcy courts, most Brazilian civil courts have very limited familiarity with corporate lending/finance – what can lead to unusual outcomes .

•ACCs, ACEs (foreign trade lines) and ‘Alienacao Fiduciaria’ – credit backed by receivables etc. emulating the legal structure of a chattel mortgage – are not subject to the ‘automatic stay’ under ‘Recuperação Judicial’ (as per Art.49 §3 of the Law and with recent backing by a decision of the Superior Court of Justice). More about this in a specific post.

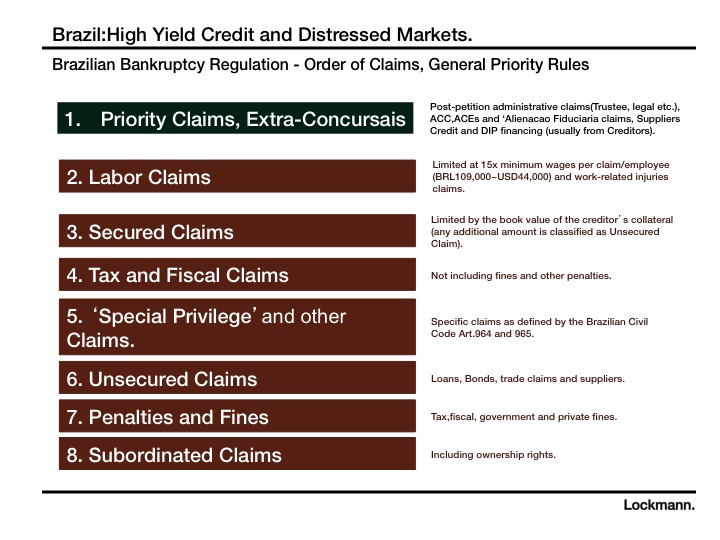

•A ‘major development’ of the (not so new now) Law was to put a cap on Labour claims (but priority over Secured Claims, continue) – please see below (click for enlarged version) – a simplified guide to the Order of Claims in a Brazilian bankruptcy case. Tax and Fiscal Claims still have seniority over Unsecured Claims.

•DIP financing is not usual in Brazil and somehow ‘untested’ – that is probably why in the OGX case – creditors decided to use foreign trade lines – to add another line of safety to their claims. Prepackaged bankruptcies are virtually non-existent.

• Fast liquidation proceedings (‘Falência’) are also not common, especially in high-profile medium/large bankruptcy cases – even in the most obvious cases, liquidations are usually postponed for as long as possible (in this case – the RJ/chapter 11 period dragged for over 5 years) – this obviously benefits the Debtor/Controlling shareholders and ‘forces’ creditors to accept a Plan of Reorganization that could be marginally better than waiting (a couple of years) for the outcome of a liquidation.

•Claims in foreign currency are automatically converted into local currency in the case of liquidation (‘Falência’) – creating immediate devaluation risk.

•The practical implications of the ‘New Brazilian Bankruptcy Law’ are being tested on a daily basis (the final outcome of the OGX/OSX case will certainly shape future cases, as it is already influencing cases like Aralco) – and potential changes to the law can happen within the discussions of the new ‘Codigo Civil” in 2014/2015.

As per usual, any corrections, feedbacks and comments are appreciated. To be continued in further posts.